|

| Pix Credit here |

The great project of convergence has been ingloriously drifting toward the trash bin of history de facto even as its once progressive now reactionary claque continues to hold high its de jure banner. Convergence was once at the heart of the vision of the world once dearly held by the Americans after 1945 as the vanguard force of the alliance victorious against the forces of global fascism (but not entirely convinced about the moral character of Soviet totalitarianism even after its bad behaviors from the late 1920s). Convergence was at the root of all progress--obliterating the effect of difference even as it increasingly and more strenuously worshiped its outward forms. Its centralizing structures were built into the structures of international organizations expressing in organizational form a modernist version of e pluribus unum. Convergence was a necessary predicate and by product of the construction of globalization.--with its toleration of national characteristics subsumed beneath a common set of ordering principles. The modern ecologies of international and regional institutions, public and private, were built to give concrete effect to this vision--the normative engines of convergence overseen by its vanguard.

But that dream of convergence is fraying. Detachment has now overtaken

the orthodox project of economic globalization. In the United States

political and constitutional de-centralization has becme a vehicle for

not merely slowing convergence but for undoing some of its signature

constitutional triumphs--for example the constitutionalization of

abortion rights. And throughout the world the basic structures and

normative foundations of public and private institutions have been

challenged for structural bias, one that suggests that convergence

itself is a source or effect or modality of bias in such structuring.

One of the last great expression of that impulse toward convergence within the operating frameworks of globalization was tied to the effort to develop a converged normative structure for human rights, and then to apply these to the conduct of economic activity in the public and private spheres. Beyond the great soft law triumphs of this movement--the UN Guiding Principles for Business and Human Rights, the ECD Guidelines for Multinational Enterprises, and the ISO 14,000 (environmental management) and 26,000 (corporate social responsibility) standards--were efforts to reconsider risk as a regulatory device and as a vessel for normative development along preferred lines. More specifically, the fundamental parameters for judging and calculating and expanding a system for embedding business risk in operational decision making in a more comprehensive and normatively significant way appeared to offer possibilities that were compatible with business practices (new wine in old bottles) but that could also transform that practice (decanting new wine into a more suitable bottle).

|

| Pix credit here |

The project of converging risk parameters had two aims (among a host of others) relevant to the reaction that was to follow nearly twenty years later. The first was to harmonize risk assessment so that risk could be better embedded in the valuation of economic activity, and more particularly investment decisions by individuals and financial institutions. The second was to develop some sort of unifying set of normative principles around which risk convergence could be rationalized. That second aim could not avoid a grounding in a specific ideology that increasingly also saw the convergence of private economic activity with the responsibility of public collectives. That, in turn, appeared to necessitate a liberation from the almost century old constraint of limiting private sector economic collectives to a primary object of purely economic value maximization. To both ends, the concepts of environmental, social (or societal), and governance (ESG) risk proved appealing as the vessel through which the responsibilities of business and economic activity could be brought broadened and embedded as a pro-active instrument of public (state) policy (beyond the mere obligation to comply with law). Both saw their current early manifestation in the work of the Global Compact, and particularly its Who Cares Wins: Connecting Financial Markets

to a Changing World.

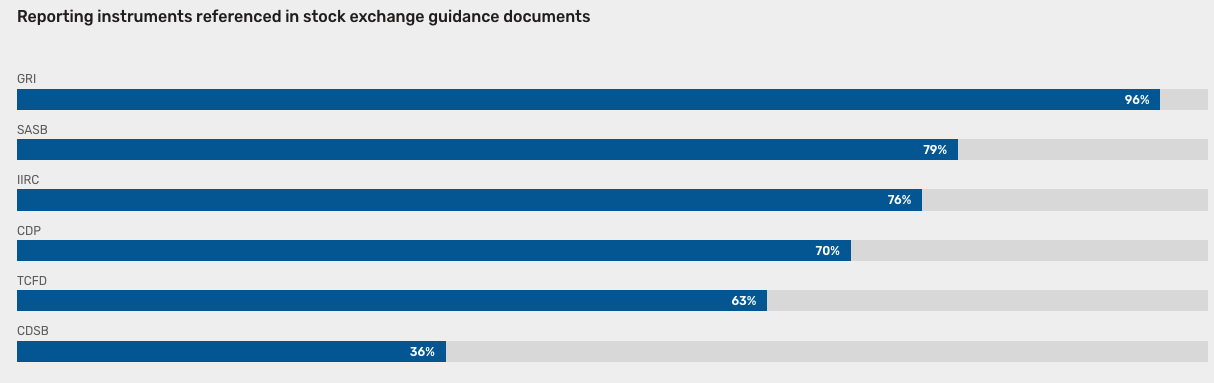

ESG remains very much a work in progress in significant respect. The European Union has sought to legalize a version that substantially expands the original notion of investment risk analysis to now embrace impacts based operational risk defined both by EU standards and their internalization of their understanding of international hard and soft norms (e.g. Corporate Sustainability Reporting Directive (CSRD) (5 January 2023 and its European Sustainability Reporting Standards (ESRS)to be developed by the EFRAG, a "private association established in 2001 with the encouragement of the European Commission to serve the public interest "; and also the Non-Financial Reporting Directive (NFRD)). Yet these legalizing efforts exist in a complex regulatory environment of hard and soft standards. Within that ecology ESG still defies definitional convergence, consensus on the valuation of risk (as well as its identification) remains unresolved. For example, it has been reported that 69 Exchanges that include ESG guidance reference six distinct standards.

|

| Pix Credit here |

And increasingly, the flexibility of definition and valuation-consequences of risk identification has proven to be irresistible as a mechanism for end running democratic or government institutional regulatory mechanisms by inserting policy priorities within the ESG process. It is in this state that ESG movement has also found itself caught in great movements that are fracturing the impulse toward global convergence of systems, valuation identification and calculation, consequential decision making and practices, and normative values.

This is very much in evidence in the United States ("The ESG Wars": Presentation of the University of Dundee (Scotland)). The global press has, of course, been following the battles between the Biden Administration and Congress over the extent to which the Federal Government may permit pension plan fiduciaries to consider ESG in their investment decisions. Less well known are efforts to encourage reporting of ESG factors by companies and discussions over the content and meaning of those terms. But it has been the invigoration of a more muscular federalism, with what appears to be a willingness by the US Supreme Court to re-imagine the division of authority between states and the national government, that is now providing substantial impetus for a vigorous debate about ESG beyond the conversations traditionally driven by elites in apex public and private institutions. Reuters recently reported that

This year state legislators, chiefly Republicans, have filed roughly 99 bills aimed at restricting the rise of ESG business practices, up from 39 in 2022, according to law firm Morgan Lewis. As of April 3, seven of the bills had been enacted into law, 20 were effectively dead, and 72 were still pending. . . ESG investing debates have taken on national significance as Democratic-aligned shareholder activists clash with Republicans increasingly adopting anti-ESG rhetoric. Some of the criticism has been harsh. Utah's Republican State Treasurer Marlo Oaks in March referred to ESG governance and to United Nations-backed sustainable development goals as "Satan’s plan" when speaking to a meeting of Republicans. The comparison with Satan was unusual. But Republicans often disparage ESG efforts with references to the global connections of top funds and characterize industry efforts like the Net Zero Asset Managers initiative as radical. (Business fights back as Republican state lawmakers push anti-ESG agenda)

|

| Pix credit here |

What do these state anti-ESG bills look like? In Mississippi, the anti-ESG bill (House Bill 818; 2023) does two things. First it adds a set of declarations to the effect that ESG criteria are unstable and ambiguous and reaffirming that ""fiduciaries may not sacrifice investment returns or assume greater investment risks as a means of promoting collateral social policy goals." It then amends Section 25-11-121(10) ,Mississippi Code of 1972, to add the following:

The board, in accordance with its fiduciary duties, shall make investment decisions with the sole purpose of maximizing the safety of, and return on, its investments. The board shall not make an investment decision with the primary purpose of influencing any social or environmental policy or attempting to influence the governance of any corporation. The board shall not sacrifice investment returns or assume greater investment risks as a means of promoting collateral social policy goals.

Florida is enacting a similar measure (see here). In early April 2023, Kansas "approved a bill that would prevent the state, its pension fund for teachers and government workers and its cities, counties and local school districts from using ESG principles in investing their funds or in awarding contracts." (Kansas passes anti-ESG bill, but it’s milder than some want).

The battling over ESG raises a number of interesting issues, most of them ignored. What is not ignored is the instrumentalization of ESG as a mechanics of delegating policy-based compliance with public regulatory oversight, contributing to the closer alignment between the regulatory apparatus of private and public organs. Regulatory oversight itself might then contribute to a weaponization of risk as a means of imposing policy determinations through technical compliance mechanisms that insulates (at times) the regulatory apparatus from democratic engagement (ironically, at its limit, itself a breach of civil and political human rights). That is the great paradox of ESG--the idea is to engage the state in the great project of mandatory ESG measures to further policy goals, but to avoid the uncertainties (and nastiness) of the democratic process toward the realization of that goal. The idea is quite profoundly brilliant--in the face of lack of consensus one can use the regulatory apparatus to train the electoral masses (and thus nudge their political representatives) toward the proper perspectives by changing the landscape in which such considerations are developed. precisely because there is no consensus yet (and thus politics in liberal democracy impedes attainment). Yet it is this quite insightful approach to mass management that sometimes produces (even if unconscious) resistance by those who shift from managers to managed in the political arena. And what appears to drive states are a cocktail of policies advanced by the Biden Administration at the core of which are climate change related measures (eg SEC Issues Sample Comment Letter as it Ramps Up Scrutiny of Climate Disclosures; State Street Global Advisors, Guidance on Climate-related Disclosures) where disclosure regimes translate into consequential ESG risk analytics. At the state level, "Conservatives have paired economic concerns. . . with Republican grievances over Biden administration climate and social policies, fueling the anti-ESG investment campaign over the past year." ('Strong, state-based network' fuels opposition to ESG investment).

In and of itself ESG is unremarkable. The business case for risk assessment was made long ago--certainly well before its current manifestation as ESG And there is nothing special about gauging business risk in valuing economic activity. What makes ESG more interesting, though, is that the risk that is being assessed is exogenous impact rather than effect on operations. Traditionally exogenous impact was treated as a public issue and compliance and risk started with legal risk (assuming that states were responsible for determine and policing tolerable (politically) levels of impact of certain forms of economic activities. Environmental laws, for example these enacted in the U.S. from the 1970s provide an example. In this sense ESG risk was a species of compliance and legal risk. To the extent there was more then it was market risk (starting perhaps with the agricultural product boycotts of the 1970s). The policy value of that mission creep, though, occurred without much debate within the political branches; it was effected through markets and in the guise of markets based technical regulation, to the extent it was embedded in public policy. On the other hand, .certainly since Who Cares Wins it has been clear that markets have developed a taste for some forms of ESG. And consent based self impositions of markets driven norms and behaviors ought to be given a substantial latitude.

At the operational level of state legislative efforts, two issues appear in large part to drive the current crop of anti-ESG measures. The first touches on control of fiduciaries. That is fair to the extent that they ought not to be driven by their own norms but are stewards for the desires and objectives of beneficiaries. Where these are state funds, then the ESG issue becomes fair game. The second is a consequences of the movement of the current debates about climate change and climate change responses from the duty of states to the responsibility of markets and economic actors (as producers of or investors in climate negative economic activity). Here the fractured politics around climate change strategies, their locus in either state organs or private sector actors, and the contests for control within divided powers states (like the United States) add substantial complexity. We have, by this point some a long way from risk and convergence models. And these debates have really only just started.

The text of the Kansas ESG Bill follows below.

CONFERENCE COMMITTEE REPORT

MR. SPEAKER and MR. PRESIDENT: Your committee on conference on Senate

amendments to HB 2100 submits the following report:

The House accedes to all Senate amendments to the bill, and your committee on conference

further agrees to amend the bill as printed with Senate Committee amendments, as follows:

On page 1, by striking all in lines 6 through 36;

On page 2, by striking all in lines 1 through 29; following line 29, by inserting:

"New Section 1. (a) The provisions of sections 1 through 6, and amendments thereto, shall

be known and may be cited as the Kansas public investments and contracts protection act. (b) As used in this act:

(1) "Act" means the Kansas public investments and contracts protection act.

(2) "Board" means the board of trustees of the Kansas public employees retirement system.

(3) "Company" means any organization, association, corporation, partnership, joint venture, limited partnership, limited liability partnership, limited liability company or other entity of business association, including a wholly owned subsidiary, majority-owned subsidiary, parent company or affiliate of such entities or business associations that exists for the purpose of making a profit. "Company" does not mean a sole proprietorship.

(4) "Environmental, social and governance criteria" means any criterion that gives preferential treatment or discriminates based on whether a company meets or fails to meet one or more of the following criteria:

(A) Engaging in the exploration, production, utilization, transportation, sale or manufacturing of:

(i) Fossil fuel-based energy;

ccr_2023_hb2100_s_2085

-2- ccr_2023_hb2100_s_2085

(ii) nuclear energy; or

(iii) any other natural resource;

(B) engaging in the production of agriculture;

(C) engaging in the production of lumber;

(D) engaging in mining;

(E) emitting greenhouse gases or not disclosing or offsetting such greenhouse gas

emissions;

(F) engaging in the manufacturing, distribution or sale of firearms, firearms accessories,

ammunition or ammunition components;

(G) having a governing corporate board or other officers whose race, ethnicity, sex or

sexual orientation meets or does not meet any criteria;

(H) facilitating or assisting or not facilitating or assisting employees in obtaining

abortions or gender reassignment services; and

(I) doing business with any company described by subparagraphs (A) through (H).

(5) "Fiduciary" means any person acting on behalf of the board or system as an

investment manager, proxy advisor or contractor, including the system's board of trustees. (6) "Fiduciary commitment" means any evidence of a fiduciary's purpose in managing assets as a fiduciary, including, but not limited to, any of the following in a fiduciary's capacity

as a fiduciary, specifically on assets managed on behalf of the system:

(A) Advertisements, statements, explanations, reports, communications with portfolio

companies, statements of principles or commitments; or

(B) participation in, affiliation with or status as a signatory to any coalition, initiative,

joint statement of principles or agreement.

(7) (A) "Financial" means having been prudently determined by a fiduciary to have a

-3- ccr_2023_hb2100_s_2085 material effect on the financial risk or the financial return of an investment.

(B) "Financial" does not include any action taken or factor considered by a fiduciary with any purpose whatsoever to further social, political or ideological interests.

(C) A fiduciary may reasonably be determined to have taken an action or considered a factor with a purpose to further social, political or ideological interests based upon evidence indicating such a purpose, including, but not limited to, any fiduciary commitment to further, through portfolio company engagement, board or shareholder votes or otherwise as a fiduciary, any of the following beyond what controlling federal or state law requires, specifically on assets managed on behalf of the system:

(i) Eliminating, reducing, offsetting or disclosing greenhouse gas emissions;

(ii) instituting or assessing corporate board, employment, composition, compensation or disclosure criteria that incorporates characteristics protected under state law;

(iii) divesting from, limiting investment in or limiting the activities or investments of any company for failing or not committing to meet environmental standards or disclosures;

(iv) accessing abortion, sex or gender change or transgender surgery; or

(v) divesting from, limiting investment in or limiting the activities or investments of any company that engages in, facilitates or supports the manufacture, import, distribution, marketing, advertising, sale or lawful use of firearms, ammunition or component parts and accessories of firearms or ammunition.

(8) "Fossil fuels" means coal, natural gas, petroleum or oil formed by natural processes through decomposition of dead organisms.

(9) "Natural resources" means fossil fuels, minerals, metal ores or any other nonrenewable or finite resource that cannot be readily replaced by natural means at the speed at which it is consumed.

-4- ccr_2023_hb2100_s_2085 (10) "System" means the Kansas public employees retirement system. "System" does

not include participant-directed individual account plans.

New Sec. 2. (a) The state, any agency of the state, any political subdivision of the state,

or any instrumentality thereof, including the pooled money investment board established by K.S.A. 75-4221a, and amendments thereto, when engaged in procuring or letting contracts for any purpose, shall ensure that bidders, offerors, contractors or subcontractors are not given preferential treatment or discriminated against based on any environmental, social and governance criteria.

(b) The state, any agency of the state, any political subdivision of the state or any instrumentality thereof, including the pooled money investment board established by K.S.A. 75- 4221a, and amendments thereto, shall not adopt any procurement regulation or policy that causes any bidder, offeror, contractor or subcontractor to be given preferential treatment or be subject to discrimination based on any environmental, social and governance criteria, except as otherwise specifically permitted or required by law.

New Sec. 3. (a) In making and supervising investments of the system, the system and any investment manager, proxy advisor or contractor thereof shall discharge its duties solely in the financial interest of the participants and beneficiaries for the exclusive purposes of:

(1) Providing financial benefits to participants and their beneficiaries; and

(2) defraying reasonable expenses of administering the system.

(b) An investment manager, proxy advisor or contractor retained by the system shall be

subject to the same fiduciary duties as the system's board of trustees.

(c) A fiduciary shall consider only financial factors when discharging such fiduciary's

duties with respect to the system.

(d) All shares held directly or indirectly by or on behalf of the system or the

-5- ccr_2023_hb2100_s_2085 participants and their beneficiaries shall be voted solely in the financial interest of system

participants and their beneficiaries.

(e) Unless no economically practicable alternative is available, the system shall not

grant proxy voting authority to any person who is not a part of the system, unless such person has a practice of, and in writing commits to, following guidelines that match the system's obligation to act solely upon financial factors, in which case the system may grant proxy voting authority to such person.

(f) Unless no economically practicable alternative is available, in the selection of any proxy advisor, the system shall give preference to a proxy advisor service that commits in writing to engage in voting shares and making recommendations in a strictly fiduciary manner, and without consideration of policy objectives that are not the express policy objectives of the system, in which case the system may engage a proxy voting advisor.

(g) Unless no economically practicable alternative is available, system assets shall not be entrusted to a fiduciary, unless such fiduciary has a practice of, and in writing commits to, following guidelines, when engaging with portfolio companies and voting shares or proxies, that follow the system's obligation to act solely upon financial factors and not upon policy considerations that are not the express policy objectives of the system, in which case the system may entrust engagement and share voting to a fiduciary.

(h) Unless no economically practicable alternative is available, an investment manager or contractor shall not, in providing service for the system, follow the recommendations of a proxy advisor or other service provider, unless such advisor or service provider has a practice of, and in writing commits to, following proxy voting guidelines that follow the system's obligation to act solely upon financial factors, in which case the investment manager or contractor may follow the recommendations of a proxy or other service advisor.

-6- ccr_2023_hb2100_s_2085 (i) All proxy votes shall be tabulated and reported annually to the system's board of trustees and to the joint committee on pensions, investments and benefits. For each vote, the report shall contain a vote caption, the system's vote, the recommendation of company management and, if applicable, the proxy advisor's recommendation. Such reports shall be

posted on the system's website for review by the public.

(j) Subsections (e) through (i) shall apply only to assets managed on behalf of the

system and shall not apply to alternative or real estate investments as defined in K.S.A. 74- 4921(5), and amendments thereto.

New Sec. 4. (a) As used in this section, "state agency" means an office, board, commission, department, council, bureau, governmental entity or other agency of state government having authority to adopt or enforce rules and regulations.

(b) No state agency shall share or publish information, adopt policies, adopt rules and regulations or issue guidelines for purposes of environmental, social and governance criteria that restrict the ability of any industry to offer products or services. No state agency shall require any person or business to adopt or operate in accordance with environmental, social and governance criteria.

New Sec. 5. (a) This act or any contract subject to this act may be enforced by the attorney general.

(b) If the attorney general has reasonable cause to believe that a person has engaged in, is engaging in or is about to engage in a violation of this act, the attorney general may require:

(1) Such person to file on such forms as the attorney general may prescribe a statement or report in writing, under oath, as to all the facts and circumstances concerning the violation; and

(2) the filing of such other data and information as the attorney general may deem

-7- ccr_2023_hb2100_s_2085

necessary.

(c) In addition to any other remedies available at law or equity, an investment manager

or contractor of the system that serves as a fiduciary and violates the provisions of section 3, and amendments thereto, shall be obligated to pay damages to the state in an amount equal to three times all moneys paid to the investment manager or contractor by the system for the services of such investment manager or contractor.

New Sec. 6. In a cause of action based on an action, inaction, decision, divestment, investment, report or other determination made or taken in compliance with this act, without regard to whether the person performed services for compensation, the state shall indemnify and hold harmless for actual damages, court costs and attorney fees adjudged against, and defend the system and any of its current and former employees, members of the board or any other officers of the system related to the act or omission on which the damages are based.

Sec. 7. K.S.A. 2022 Supp. 74-4921 is hereby amended to read as follows: 74-4921. (1) There is hereby created in the state treasury the Kansas public employees retirement fund. All employee and employer contributions shall be deposited in the state treasury to be credited to the Kansas public employees retirement fund. The fund is a trust fund and shall be used solely for the exclusive purpose of providing benefits to members and member beneficiaries and defraying reasonable expenses of administering the fund. Investment income of the fund shall be added or credited to the fund as provided by law. All benefits payable under the system, refund of contributions and overpayments, purchases or investments under the law and expenses in connection with the system unless otherwise provided by law shall be paid from the fund. The director of accounts and reports is authorized to draw warrants on the state treasurer and against such fund upon the filing in the director's office of proper vouchers executed by the chairperson or the executive director of the board. As an alternative, payments from the fund may be made by

-8- ccr_2023_hb2100_s_2085 credits to the accounts of recipients of payments in banks, savings and loan associations and credit unions. A payment shall be so made only upon the written authorization and direction of the recipient of payment and upon receipt of such authorization such payments shall be made in

accordance therewith. Orders for payment of such claims may be contained on:

(a) A letter, memorandum, telegram, computer printout or similar writing,; or

(b) any form of communication, other than voice, which is registered upon magnetic

tape, disc or any other medium designed to capture and contain in durable form conventional signals used for the electronic communication of messages.

(2) The board shall have the responsibility for the management of the fund and shall discharge the board's duties with respect to the fund solely in the interests of the members and beneficiaries of the system for the exclusive purpose of providing benefits to members and such member's beneficiaries and defraying reasonable expenses of administering the fund and shall invest and reinvest moneys in the fund and acquire, retain, manage, including the exercise of any voting rights and disposal of investments of the fund within the limitations and according to the powers, duties and purposes as prescribed by this section.

(3) Moneys in the fund shall be invested and reinvested to achieve the investment objective which is preservation of the fund to provide benefits to members and member beneficiaries, as provided by law and accordingly providing that the moneys are as productive as possible, subject to the standards set forth in this act. No moneys in the fund shall be invested or reinvested if the sole or primary any investment objective is for economic development or social purposes or objectives.

(4) In investing and reinvesting moneys in the fund and in acquiring, retaining, managing and disposing of investments of the fund, the board shall exercise the judgment, care, skill, prudence and diligence under the circumstances then prevailing, which persons of

-9- ccr_2023_hb2100_s_2085 prudence, discretion and intelligence acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of like character and with like aims by diversifying the investments of the fund so as to minimize the risk of large losses, unless under the circumstances it is clearly prudent not to do so, and not in regard to speculation but in regard to the permanent disposition of similar funds, considering the probable income as well as the probable safety of

their capital.

(5) Notwithstanding subsection (4):

(a) Total investments in common stock may be made in the amount of up to 60% of the

total book value of the fund;

(b) the board may invest or reinvest moneys of the fund in alternative investments if the

following conditions are satisfied:

(i) The total of the annual net commitment to alternative investments does not exceed

5% of the total market value of investment assets of the fund as measured from the end of the preceding calendar year;

(ii) if in addition to the system, there are at least two other qualified institutional buyers, as defined by section (a)(1)(i) of rule 144A, securities act of 1933;

(iii) the system's share in any individual alternative investment is limited to an investment representing not more than 20% of any such individual alternative investment;

(iv) the system has received a favorable and appropriate recommendation from a qualified, independent expert in investment management or analysis in that particular type of alternative investment;

(v) the alternative investment is consistent with the system's investment policies and objectives as provided in subsection (6);

(vi) the individual alternative investment does not exceed more than 2.5% of the total

-10- ccr_2023_hb2100_s_2085 alternative investments made under this subsection. If the alternative investment is made pursuant to participation by the system in a multi-investor pool, the 2.5% limitation contained in this subsection is applied to the underlying individual assets of such pool and not to investment in the pool itself. The total of such alternative investments made pursuant to participation by the system in any one individual multi-investor pool shall not exceed more than 20% of the total of alternative investments made by the system pursuant to this subsection. Nothing in this subsection requires the board to liquidate or sell the system's holdings in any alternative investments made pursuant to participation by the system in any one individual multi-investor pool held by the system on the effective date of this act, unless such liquidation or sale would be in the best interest of the members and beneficiaries of the system and be prudent under the standards contained in this section. The 20% limitation contained in this subsection shall not have been violated if the total of such investment in any one individual multi-investor pool exceeds 20% of the total alternative investments of the fund as a result of market forces acting to increase the value of such a multi-investor pool relative to the rest of the system's alternative investments; however, the board shall not invest or reinvest any moneys of the fund in any such individual multi-investor pool until the value of such individual multi-investor pool is less than

20% of the total alternative investments of the fund;

(vii) the board has received and considered the investment manager's due diligence

findings submitted to the board as required by subsection (6)(c) (6);

(viii) prior to the time the alternative investment is made, the system has in place

procedures and systems to ensure that the investment is properly monitored and investment performance is accurately measured; and

(ix) the total of alternative investments does not exceed 15% of the total investment assets of the fund. The 15% limitation contained in this subsection shall not have been violated if

-11- ccr_2023_hb2100_s_2085 the total of such alternative investments exceeds 15% of the total investment assets of the fund, based on the fund total market value, as a result of market forces acting to increase the value of such alternative investments relative to the rest of the system's investments. However, the board shall not invest or reinvest any moneys of the fund in alternative investments until the total value of such alternative investments is less than 15% of the total investment assets of the fund based on the market value. If the total value of the alternative investments exceeds 15% of the total investment assets of the fund, the board shall not be required to liquidate or sell the system's holdings in any alternative investment held by the system, unless such liquidation or sale would be in the best interest of the members and beneficiaries of the system and is prudent under the

standards contained in this section.;

(c) for purposes of this act section, "alternative investment" includes a broad group of

investments that are not one of the traditional asset types of public equities, fixed income, cash or real estate. Alternative investments are generally made through limited partnership or similar structures, are not regularly traded on nationally recognized exchanges and thus are relatively illiquid, and exhibit lower correlations with more liquid asset types such as stocks and bonds. Alternative investments generally include, but are not limited to, private equity, private credit, hedge funds, infrastructure, commodities and other investments which that have the characteristics described in this paragraph; and

(c)(d) except as otherwise provided, the board may invest or reinvest moneys of the fund in real estate investments if the following conditions are satisfied:

(i) The system has received a favorable and appropriate recommendation from a qualified, independent expert in investment management or analysis in that particular type of real estate investment;

(ii) the real estate investment is consistent with the system's investment policies and

-12- ccr_2023_hb2100_s_2085 objectives as provided in subsection (6); and

(iii) the system has received and considered the investment manager's due diligence findings.

(6) (a) Subject to the objective set forth in subsection (3) and the standards set forth in subsections (4) and (5) the board shall formulate policies and objectives for the investment and reinvestment of moneys in the fund and the acquisition, retention, management and disposition of investments of the fund. Such policies and objectives shall include:

(a)(i) Specific asset allocation standards and objectives;

(b)(ii) establishment of criteria for evaluating the risk versus the potential return on a particular investment;

(c)(iii) a requirement that all investment managers submit such manager's due diligence findings on each investment to the board or investment advisory committee for approval or rejection prior to making any alternative investment;

(d)(iv) a requirement that all investment managers shall immediately report all instances of default on investments to the board and provide the board with recommendations and options, including, but not limited to, curing the default or withdrawal from the investment; and

(e)(v) establishment of criteria that would be used as a guideline for determining when no additional add-on investments or reinvestments would be made and when the investment would be liquidated.

(b) The board shall review such policies and objectives, make changes considered necessary or desirable and readopt such policies and objectives on an annual basis.

(7) The board may enter into contracts with one or more persons whom the board determines to be qualified, whereby the persons undertake to perform the functions specified in

-13- ccr_2023_hb2100_s_2085 subsection (2) to the extent provided in the contract. Performance of functions under contract so entered into shall be paid pursuant to rates fixed by the board subject to provisions of appropriation acts and shall be based on specific contractual fee arrangements. The system shall not pay or reimburse any expenses of persons contracted with pursuant to this subsection, except that after approval of the board, the system may pay approved investment related expenses subject to provisions of appropriation acts. The board shall require that a person contracted with to obtain commercial insurance which provides for errors and omissions coverage for such person in an amount to be specified by the board, provided that such coverage shall be at least the greater of $500,000 or 1% of the funds entrusted to such person up to a maximum of $10,000,000. The board shall require a person contracted with to give a fidelity bond in a penal sum as may be fixed by law or, if not so fixed, as may be fixed by the board, with corporate surety authorized to do business in this state. Such persons contracted with the board pursuant to this subsection and any persons contracted with such persons to perform the functions specified in subsection (2) shall be deemed to be agents of the board and the system in the performance of

contractual obligations.

(8) (a) In the acquisition or disposition of securities, the board may rely on the written

legal opinion of a reputable bond attorney or attorneys, the written opinion of the attorney of the investment counselor or managers, or the written opinion of the attorney general certifying the legality of the securities.

(b) The board shall employ or retain qualified investment counsel or counselors or may negotiate with a trust company to assist and advise in the judicious investment of funds as herein provided.

(9) (a) Except as provided in subsection (7) and this subsection, the custody of money and securities of the fund shall remain in the custody of the state treasurer, except that the board

-14- ccr_2023_hb2100_s_2085 may arrange for the custody of such money and securities as it considers advisable with one or more member banks or trust companies of the federal reserve system or with one or more banks in the state of Kansas, or both, to be held in safekeeping by the banks or trust companies for the collection of the principal and interest or other income or of the proceeds of sale. The services provided by the banks or trust companies shall be paid pursuant to rates fixed by the board

subject to provisions of appropriation acts.

(b) The state treasurer and the board shall collect the principal and interest or other

income of investments or the proceeds of sale of securities in the custody of the state treasurer and pay same when so collected into the fund.

(c) The principal and interest or other income or the proceeds of sale of securities as provided in clause (a) of this subsection (9) shall be reported to the state treasurer and the board and credited to the fund.

(10) The board shall with the advice of the director of accounts and reports establish the requirements and procedure for reporting any and all activity relating to investment functions provided for in this act in order to prepare a record monthly of the investment income and changes made during the preceding month. The record will reflect a detailed summary of investment, reinvestment, purchase, sale and exchange transactions and such other information as the board may consider advisable to reflect a true accounting of the investment activity of the fund.

(11) The board shall provide for an examination of the investment program annually. The examination shall include an evaluation of current investment policies and practices and of specific investments of the fund in relation to the objective set forth in subsection (3), the standard set forth in subsection (4) and other criteria as may be appropriate, and recommendations relating to the fund investment policies and practices and to specific

-15- ccr_2023_hb2100_s_2085 investments of the fund as are considered necessary or desirable. The board shall include in its annual report to the governor as provided in K.S.A. 74-4907, and amendments thereto, a report

or a summary thereof covering the investments of the fund.

(12) (a) Any internal assessment or examination of alternative investments of the

system performed by any person or entity employed or retained by the board which evaluates or monitors the performance of alternative investments shall be reported to the legislative post auditor so that such report may be reviewed in accordance with the annual financial-compliance audits conducted pursuant to K.S.A. 74-49,136, and amendments thereto.

(b) The board shall prepare and submit an alternative investment report to the joint committee on pensions, investments and benefits prior to January 1, 2016. Such report shall include a review of alternative investments of the system with an emphasis on the effects of changes in law pursuant to this act and includes specific investment cost and market value information of each individual alternative investment.

Sec. 8. K.S.A. 2022 Supp. 74-4921 is hereby repealed.";

Also on page 2, in line 31, by striking "Kansas register" and inserting "statute book";

And by renumbering sections accordingly;

On page 1, in the title, in line 1, by striking all after "concerning"; by striking all in line 2;

in line 3, by striking all before the period and inserting "environmental, social and governance criteria involving public contracts and investments; enacting the Kansas public investments and contracts protection act; prohibiting the state or a political subdivision from giving preferential treatment to or discriminating against companies based on environmental, social and governance criteria in procuring or letting contracts; requiring fiduciaries of the Kansas public employees retirement system to act solely in the financial interest of participants and beneficiaries of the system; restricting state agencies from adopting environmental, social and governance criteria or

-16- ccr_2023_hb2100_s_2085 requiring any person or business to operate in accordance with such criteria; providing for enforcement of such act by the attorney general; indemnifying the Kansas public employees retirement system with respect to actions taken in compliance with such act; amending K.S.A.

2022 Supp. 74-4921 and repealing the existing section";

And your committee on conference recommends the adoption of this report.

___________________________

___________________________

___________________________ Conferees on part of Senate

___________________________

___________________________

___________________________ Conferees on part of House

No comments:

Post a Comment