It is my great pleasure to announce an upcoming conference: The Future of Sovereign Wealth Funds, sponsored by the Wake Forest Law Review 2017 as their Spring Symposium. For conference information please see HERE.

This post includes the Conference Program and summary observations on each of the presentations, all of which follow, below.

Wake Forest Law Review 2017 Spring Symposium

9 a.m. Dean’s Welcome

Dean Suzanne Reynolds, Dean, Wake Forest University School of Law

A very gracious welcome from the Dean. Noted that the focus of these symposium was to look at emerging business issues, of which this was an important element.

9.10 a.m. Introductory Remarks

Alan Palmiter, Howard L. Oleck Professor of Business Law, Wake Forest University School of Law

He offered context for the symposium, identified the questions that the panelists would pose during the course of the day, and lastly put SWFs in the context pf the global economy. The focus on SWFs is intimately tied to earlier consideration of climate change (2009), the sustainable corporation (2011), the viability of agency costs (2013), and lastly the role of emerging financial intermediaries (2015). Putting this together, it only made sense to fill this out with the mixed public private nature of state activity that injects itself into private global financial markets. To that end one needs look at the legal framework and its genesis in soft law, considering the special nature of these funds, and the shift of their investment from investment to strategic development. One also needs to consider the ends ro which they are used to further global projects of sustainable business and finance, and governance (of states). He starts with the great Chiffrephile Angus Maddison in Gronigen. He looked at human wealth, which he noted was stuck at about $1 trillion. All this changed in 1800 when human wealth began to grow, human population surged along with it. The growth was fast and large. But wealth creation has not been uniform--with North American leading Europe and Asia. What led to this transformation: industrialism and mass production, growing food production, advances in sanitation, technological innovation and growth in leisure permitting even greater rates of creativity, huge gains in productivity. The trigger was the aggregation of people and capital represented by the corporation. Their investment in capital intensive business leveraged capital to produce vast wealth. But externalities, positive and negative, to the point that success puts civilization at risk. Markets are oblivious to environmental changes because of the way they have been set up; failures to account for full economic value of production has shifted its costs to those least able to bear them. It is in this context that SWFs became an interesting bridge and a metaphor for the changes in global finance and production that marks the current age.

9.20 a.m. The Role and Future of Sovereign Wealth Funds: A Trade and Investment Perspective

Locknie Hsu, Professor of Law, Singapore Management University.

She spoke to SWFs, their character and the legal framework within which they are now managed. Painted a broader brush picture of observations of SWFs in the context of hard and soft law regimes. She started with a brief history of the SWF and noted their variation and objectives and then moved to their legal treatment. She asserted that they are creatures in search of legal identity. She noted the difficulty of categorization and the complications of the political issues that targeted SWFs int he course of the Great Recession.Their character remains elusive: state owned yet private, state capitalism in a private markets oriented capitalism regime. One basic definition was put forward through the Santiago Principles--which serves as a useful default working definition. Legal regulation falls into three baskets: governance initiatives (OECD Guidelines on SOEs, Santiago Principles, etc.); national investment laws with national security dimensions (host states); and investment treaties.The first goes to institutionalization and behavior norms, the second goes to hist state chokepoint rules and the third goes to strategic behavior among states. With respect to BITs and FTAs she noted the way that SWFs and SOEs are treated in similar ways (that is to the extent that there are instances where regulatory provisions could apply to both)--in both cases of course they represent projections of state financial power abroad. Issue if their treatment--are they states for ICSID arbitration under BITs or private enterprises (ICSID Rev. 31(1):24-35 (2016). She also considered the trilateral investment agreement (China, Korea and Japan) where the parties agreed that SWFs could be treated as "investors" under investment treaty definitions (not as Contracting Parties which is very different). She noted TPP Annex 17-E and 9-H and the Canada -EU FTA (investment review decisions excluded from investor-State dispute settlement). Us-Singapore FTA 2004 speaks to SWFs to exclude them from certain provisions (Chp 12 excluding SWFs from covered entities). She ended with the emerging multidimensionality of SWFs as social policy and governance enhancing vehicles (Santiago Principle's 18-19; China's new Silk Road Fund).

9.45 a.m. Sovereign Wealth Fund Transparency and Accountability

Edwin Truman, Senior Fellow, Peterson Institute for International Economics

Transparency and accountability are central to SWF functionality. He started with background especially the concerns and suspicions of these devices that came to a head with the Great Recession. That precipitated his idea to develop an SWF Scoreboard consisting of 33 elements to measure the transparency and accountability of SWF (predating Santiago Principles). The 4th Scoreboard was produced in 2016. The 1st Scoreboard looked at 37 funds in 31 states; constricted as a benchmark. "015 Scoreboard looked at 60 funds form 43 states. Each Scoreboard has revealed substantial differences in transparency and accountability, but in aggregate substantial improvement. New funds average 56, range 77 to 33. Six US Funds average 79. Bottom line--don't generalize. The Scoreboard itself includes 33 elements grouped into 4 categories: stricture, governance, transparency and accountability, and behavior. Most progress cane in the 2007-2009 gap and between 2012 to 2015 gap. Why? Thus the main object of the presentation: explore the nature of the relationship between transparency and accountability and then explores sources on influence on differences and changes in scores. Accountability and Transparency: transparency is a necessary but not sufficient condition for accountability. Can one distinguish between transparency and accountability elements? Chart the relationship between Governance (Y) and T&A and Behavior (X) and also between refined structure and governance (Y) and Refined T&A. Accountability significantly positively related to transparency. Refined measures more powerfully related but the difference is not significant. Further refinement yields much weaker relationship. Conclusion: Scoreboard can't really different between T & A elements, and are measuring only the potential for greater accountability. With 2105 scores (internal pressures) consider SWF score (Y) on WGI Gov't Effectiveness (X) and SWF Score (Y) and WGI Voice and Accountability (X)Scores were positively related to both measures of internal pressure. External pressure: scores positively related to both size of SWF and share of foreign assets. Butt he relationships are far form significant. Are there better indicator? Looked to peer pressure. IFSWF members consistently scored higher on average than non members but the pap has not narrowed and progress is similar in terms of the size and incidence of the 2007-09 change and the 2012-15 change. So, is IFSWF membership a valuable indicator? Conclusions: internal pressure , yes but need to look at other indicators; external pressure not.

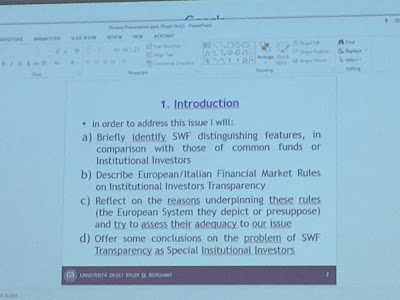

10.10 a.m. The Problem of Sovereign Wealth Fund Transparency in European Union Financial Markets: The European Rules on Institutional Investors and the Italian Perspective

Enrico Ginevra, Professor of Law, University of Bergamo

10.35 a.m. Morning Break

He addressed the question of transparency form different point of view. He looks to the question of transparency for special institutional investors like SWFs, special int he sense that their transparency has potential influence on other investments by other actors. He identified SWF distinguishing features, describe the European Italian framework and the reasons underpinning these rules, and then offer conclusions. SWFs are long term investors and care about long term income. Do not follow "Wall Street Rules"; no interest on controlling entities in which they invest. No strict fiduciary relationship in which there is a full empowerment in private funds; the relationship is more contractual than organizational and there is a special internal agency relationship among the government organs which shares responsibility. European legal framework was then explored. Found that there was a low level of portfolio exposure compared to US (eg transparency). On disclosure a low level of working policy disclosure--prefer generalized to specific disclosures and even when requested only in general terms (EU 2013 rules). No equivalent to US Rule 13D though some move toward small block investment disclosure. How does one assess the level of European transparency rules applicable to SWFs? Insufficient with low level of accountability for asset managers. But does this have relevancy of the problem given the agency of agency relationship between the fund and its owner. This may be shooting at wrong target. The real question is the level of transparency either to the polity of SWF home states or generally of transparency to the markets within which SWFs function. But even information of intentions on control of 5% blockholders is less relevant especially given patterns of shareholding in Europe. Controlling European companies is more stable (or was) and therefore he suggested these information might even at times be misleading. So, what information ought to be disclosed? monitoring based--against negligence; against breach of fiduciary duty (private appropriation of benefit) and the like. Thus the conclusion: supplementary regulations are needed, Santiago Principles insufficient. But new regulations are coming: Shareholder Directive of 2007 (especially ¶ 3(f) and 3(g)). Yet there are problems: will it apply to SWFs (maybe not); final shift of transparency issue from Law of Investment to the law of listed corporations that is part of modern shift from prudence to rules on sustainable competition. Still the search for transparency vehicles must continue as key of participation of SWF to competitive socio-economic processes.

10.35 a.m. Morning Break

10.55 a.m. U.S. Financial Regulation of Sovereign Wealth Funds

David Freeman, Partner, Arnold & Porter Kaye Scholer

He offered us a host state perspective and their regulatory responses to SWF investments. Federal banking, securities, commodities and systemic risk regulations. Will not speak to parallel state systems of regulation that may apply. SWFs tend to be the "unprovided for case in many respects with few exceptions. What is new is the regulation of swaps and other transactions. First he looked to definitions of SWFs--this critical for figuring out the classes of transactions subject to law. For him these include exclusively government owned and controlled pools of assets (not include reserves, or the sovereign itself). But sometimes definitions can be used strategically to broaden or narrow the regulatory scope. Sometimes hard to separate the sovereign from its pools of money, especially where these pools are not segregated into separate legal entities. Regulations tailored to sovereigns issuing securities or debt--they are buying things so don't get picked up by laws regulating issuers. Differentiated from sovereigns because of the way US applies its law of comity for sovereigns. Start with assumption that sovereign activities are beyond law--exception are the baroque rules and case law touching on commercial activities. US financial regulatory system is an alphabet soup of regulations that may or may not be coordinated. SWFs came on the radar at the same time as derivatives and the financial crisis. That convergence led to Dodd-Frank and a lot of political attention paid to foreign sovereign investors (Congressional hearings, etc.); SEC looking for assurance that these investments were primarily driven by profit, concerned about political influence and use of inside information. Monitoring 13f filings. CFTC on the other hand looked to the protection of underlying commodities against markets distortion--for them profit maximizing was not a good thing. Also now look for systemic risk for SWF--is the fund itself a risk, does it amplify risk--data gathering. One big area of securities law--what investments are suitable for particular investors. Reason by analogy--treat them like their private analogue. Where there are difficulties at CFTC who can be a swap dealer positing regulation by exemption (SWF treated like a hedge fund in some cases). Money laundering and foreign corrupt practices act can also apply.

11.20 a.m. International Relations and Sovereign Wealth Funds’ Political Value: Evidence from a Quasi-Natural Experiment

William Megginson, Professor and Price Chair in Finance, University of Oklahoma Michael F. Price College of Business

He considers the future of SWFs and their political value. Starts with definitions with reference to the Kuwait Investment Authority (1953) and then the Truman definition (2008) separate pool of funding that includes international assets, to a number of other definitions which range from very broad to very narrow (Sovereign Investment Laboratory). SWFs have been buying more than selling, however you define them. Query: are they an economic threat? Depends on how you view the sovereign character of investing abroad. Focus on the political ambiguity of SWFs--political agenda or just folks investors, with conflicting research results. They tend to be quite passive but some suggest some political agenda. Is there a SWF discount and here (conflicting evidence). Have SWFs influenced or been influenced by the 2016 US elections? Three criteria-Unexpected; yes. Had massive effect on financial markets with a straight shot up. Did it change expected future IR? Yes foreshadowing major changes. Were the effects expected to be heterogeneous? Yes. He then pointed to SWF data identifying what SWF owned in certain US stocks before and after the election.What happened? (Cumulative abnormal effects) Stocks with SWF investment went down by 4% when generally others went up 2%. Conclusion market reacted very negatively to stock with SWF shareholders. International relations priced in the market. Presented some evidence that they are.

11.45 a.m. Sovereign Wealth Management 2.0: Financing Growth and National Competitiveness

Patrick Schena, Adjunct Assistant Professor of International Business Relations, Tuft University Fletcher School

He spoke to the role of sovereign investors and the sovereign investment model. Aim is to rethink the SWF paradigm (scarce capital versus surplus; capital poor states investing in foreign markets; appropriate role for the state int he national economy; industrial policy; the state as capitalist; SWF as passive investors; capitalization, mandate and governance). Spoke to the rationale for foreign investment (insulate domestic economy from negative macro impacts; serve as volatility buffer etc,.). He noted that domestic mandates are development or strategic (manage or privatize sovereign assets (the Singapore funds), develop domestic sectors, infrastructure build out, promote strategic investment). He suggested the range of development mandates and institutional structures. And he noted that innovation is coming to these models. So what of the future of SWF? It is not about futures funds but a proliferation of funds focused on strategic development. He noted the "paradox of scarcity," noting that many states that use SWFs do not have much by way of surpluses (e.g., Turkey and its SWF made up of transfers of Turkish SOEs) use their assets to collateralize their assets for investment to draw capital in to restart economic engine. Who is buying this? Yet this suggests innovation in using assets and financial mechanisms for wealth creation through the instrumentalities of the state. Paradigm shifts becase SWFs become the object of inward capital in these countries so that the transparency of the SWF to co investors and others become very important to encourage the inflow of capital on a continuing and sustainable basis. How to move from traditional state capital to private investment model? He ended by suggesting moves toward an operating protocol. Target both competitive financial returns and development impact; projects generate non concessionary investment returns; provide ancillary services; catalyze crowd in direct investment (co-investment); exhibit strong governance; insulation from political pressure; multi tier accountability; flexible investment structures; dependence on ability to develop and retain domestic capacity, etc.

12.10 p.m.Lunch: Reynolda Hall, Autumn Room, 2nd Floor

Presenters, Wake Forest Law School professors, and Law Review Editors

1.30 p.m. Investing in Sustainability or Feeding on Stranded Assets? e Norwegian Government Pension Fund Global

Beate Sjåjell, Faculty of Law, University of Oslo

She posits that access to finance is crucial if we are to achieve the fundamental transition necessary to meet the grand challenge of our time: securing a safe and just operating within the planetary boundaries. To that point she undertakes a case study of the world’s largest Sovereign Wealth Fund (SWF), the Norwegian Government Pension Global. She notes that SWFs offer one of the few public economic institutions capable of injecting ecological and social values into global markets, and the Norway SWF is a good example of this type. She started with a brief history of the Norway SWF and its financial model. The SWF can only invest abroad (of course there is another fund in Norway that invests domestically and regionally). She noted its institutionalization fo ethics based investing through a set of Ethics Guidelines, the Ethics COuncil and the authority of Norges Bank to enforce the investment universe exclusion and observation rules. She then turned to discuss the Norway SWFs' mandate and whether the general management of the fund reflects the financial risk evaluation that is meant to be an integrated element in a long term, sustainability-oriented perspective. She also considered the SWF's engagement with and potential withdrawal from companies, querying whether the informational basis for the Fund’s decisions is relevant, reliable and verifiable. She asks: is the Norway SWF in practice is more reactive rather than proactive, responding to public opinion and media controversy when considering divestment, rather than undertaking due diligence beforehand and continuously monitoring its investments? The controversial North Dakota pipeline was discussed as part of a broader inquiry of whether institutional design can assure investments that contribute to sustainability, often referred to as Socially Responsible Investment (SR), or whether the power of global markets, capitalism and other drivers of the Anthropocene are too strong for any institutional design to overcome.

1.55 p.m. Sovereign Wealth Funds Investing in Germany: Public Policy-Restrictions or Free Movement of Capital?

Marc-Philippe Weller, Professor of Law, Heidelberg University

He considered SWF investing in Germany. He critically reviewed the changes made to the German Foreign Trade and Payments Act (FTPA) and its related Foreign Trade Payments Ordinance (FTPO) in 2009. These provide a basis for state review of proposed investments on public policy or security grounds. He questions the compatibility of this regime with core EU market freedoms. (especially article 63 TFEU free movement of capital) He argues that the provisions of free movement of capital are applicable and concludes that the vagueness of the provisions of the FTPA ultimately violates EU Law. In that connection he raises a number of propositions. First that the freedom of establishment (Art. 49) which doe snot offer any protection for 3rd country nationals does not supersede the fundamental freedom of capital in Art. 63(1). Second, the national legislation at issue is not sufficiently clear. A "dynamic reference" to the European Court of Justice would not suffice to clarify the legislation, so that the national legislation itself must be required to define concretely the scope of its coverage. Third, in any case the FTPA violates EU jurisprudence principals of proportionality. Its application goes beyond what is necessary to protect public policy and security. That can be remedied by enumerating the specific sectors to which it is applicable and by defining the criteria to be used when an investment in these sectors threatens public policy and security.

2.20 p.m. What Responsibilities Do Sovereign Funds Have to Other Investors?

Paul Rose, Frank E. and Virginia H. Bazler Designated Professor in Business Law, Ohio State University Moritz College of Law

He argued for a sovereign investors to recognize the special responsibilities they have to other investors. Although they should not receive any more regulatory scrutiny than other investors, assuming they are acting appropriately, their market power and connection to the larger government (even if they enjoy—as they should—a large amount of autonomy) call for a sense of responsibility that sovereign funds should embrace. To that end he spoke to issues of the responsibilities of SWFs, investor obligations and then to the way that the Santiago Principles may be useful in that discussion. He started by considering the scope and utility of fiduciary duty and its universal application under a variety of guises. He considered the way these appear within the objectives of the Chinese Fund even when the language of fiduciary duty does not directly appear. He then considers to whom is the duty owed. First of course, the government. But what does that mean--the citizens, the voters, the elites or the institutional apparatus of the state, future generations? He assumes that the state itself is a fiduciary state, that is that the state itself is a fiduciary for its citizens. This illustrates the common agency problem. The problem might be ameliorated through application of principles, some of which might be found in the Santiago Principles, though they fall far short. These are principles of transparency, predictability and presence.

2.45 p.m. Afternoon Break

3.05 p.m. Sovereign Wealth Funds, Capacity Building, Development, and Governance

Larry Catá Backer, W. Richard and Mary Eshelman Faculty Scholar, Penn State Law

3.30 p.m. Sovereign Wealth and Social Responsibility

Chris Thomale, Professor of Law, University of Heidelberg

Closing Remarks

Larry Catá Backer, W. Richard and Mary Eshelman Faculty Scholar, Penn State Law

The paper considers the way that SWFs may be transformed by and are transforming the framework of global finance and production relationships. SWFs have already started moving well beyond their idealized form, established within the parameters of the Santiago Principles. SWFs now advance the political and economic projects of states, they serve to strengthen governance, they are the focal point for the normalization of global human rights in economic activities projects, and they also serve to advance the development goals of states. The old issues of the commercial character of these mechanisms, and of their effects of the financial markets and ownership structures of rich home states remains important, but may no longer be the central element pushing the development of SWFs. Law and regulatory structures lag far behind the realities that are taking shape on the ground. The public-private divide, the constraining structures of national principles of taxation and sovereign immunity are now ripe for contestation and change. But on what basis? More HERE. PowerPoint HERE.

3.30 p.m. Sovereign Wealth and Social Responsibility

Chris Thomale, Professor of Law, University of Heidelberg

He started by considering the implications of incoherence in approaches to SWFs starting with our understanding of what one is. When does a fund start and stop being an SWF in a fluid context in which investment and ownership may be fluid. Compounded with the blurring of the public-private divide, he suggests that we have to redirect our efforts and fix certain externalities in our corporate and economic systems rather than cheery picking certain players around which regulatory systems are built. That require us to think more broadly. Yet applying human rights to the business of SWFs may not be the way to go either. He then considered the UN Guiding Principles for Business and Human Rights in this respect and wonders whether the difference between the state duty pillar and the corporate responsibility pillar is as useful where the public and private spheres are now less distinct.Should revisits corporate and capital markets law instead. Thus the current approach seems to put the cart before the horse. Rather rethinking capital markets in light of its objectives and the duties of enterprises and business behavior generally might be a more efficient way to deal with a problem that is really only a specific instance of a more general set of challenges.

Closing Remarks

No comments:

Post a Comment